As published on The Success Bug Website

Currently, new COVID-19 cases are surging across the country, the fate of a second stimulus check seems unlikely, and benefits are running out. These recent events have been stressful for all Americans. However, for Generation Z, this is an especially taxing time as many have just graduated college or have been part of the first wave of corporate layoffs.

Right now, you may be looking at your budget and thinking, “There’s no way I can spend any less money!” But the fact is that even the most frugal people can find additional ways to cut down on their bills.

And no, I am not going to say you need to cancel your cable bill and eat ramen noodles every day. Saving money doesn’t have to come at a huge sacrifice to your current way of life. But the reason why it’s so important to save, especially for Gen Zs, is because you have the majority of your life in front of you. If you can get in the right habits now to save money, then down the road, things like weddings, kids, and retirement won’t seem like such a financial burden. In this post, you will learn the 10 easiest ways to start saving money.

1. Cut All Unnecessary Subscriptions

Waterstone Management Group found that 84% of Americans grossly underestimate what they spend on their subscriptions every month. When we think of subscriptions, we mainly just think of the most popular ones, like Netflix, Spotify, Dollar Shave Club, and Amazon. What we forget are the other subscriptions that may be eating away at our savings.

When looking at a more exhaustive list of subscription services, you quickly realize that you may be spending hundreds of dollars on things such as iPhone apps, gaming services, newspaper & magazine subscriptions, meal kits, gym memberships, and more.

First, you’re going to want to download Truebill, an app that easily allows you to view and cancel unwanted subscriptions. Cancel all the subscriptions that you don’t use anymore. Then you’re going to focus on the 20% of your subscriptions that lead to the majority of your costs. This is where you’re going to find the greatest cost savings.

Look at these few subscriptions and try to find cheaper alternatives. Maybe you don’t need a gym with a sauna in it and can find a regular one for half the monthly cost. If you don’t have to shave frequently, change your Dollar Shave Club membership from coming every month to every other month.

2. Create A Budget

“Alice asked the Cheshire Cat, who was sitting in a tree, “What road do I take?”

The cat asked, “Where do you want to go?”

“I don’t know,” Alice answered.

“Then,” said the Cat, “it really doesn’t matter, does it?”

― Lewis Carroll, Alice’s Adventures In Wonderland

What does this quote symbolize other than an iconic line from Alice in Wonderland? It means it doesn’t matter what you do if you don’t know where you want to end up. This is why you must create a budget for yourself. A budget will keep you on track with spending goals and provide a definitive end goal.

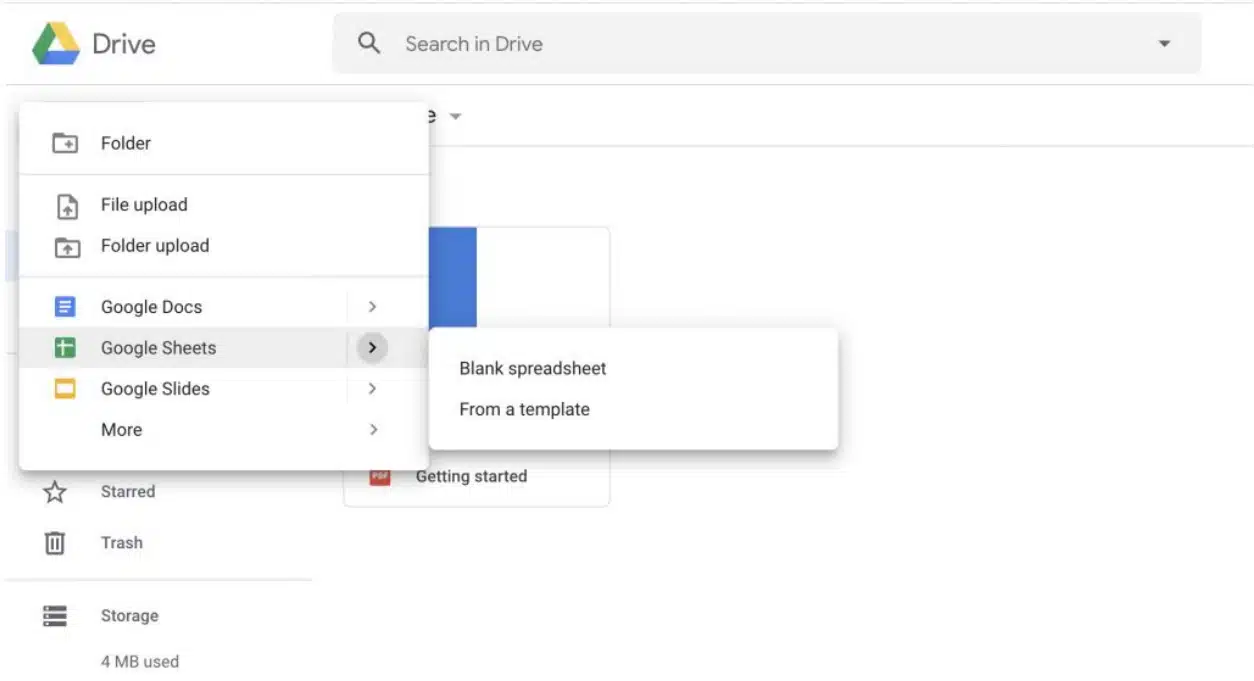

My favorite tool for keeping track of my expenses is the pre-built templates from Google Sheets. Once you enter your Google Drive, you can go to the top left corner, click “New,” scroll down to Google Sheets, and select, “From a template.”

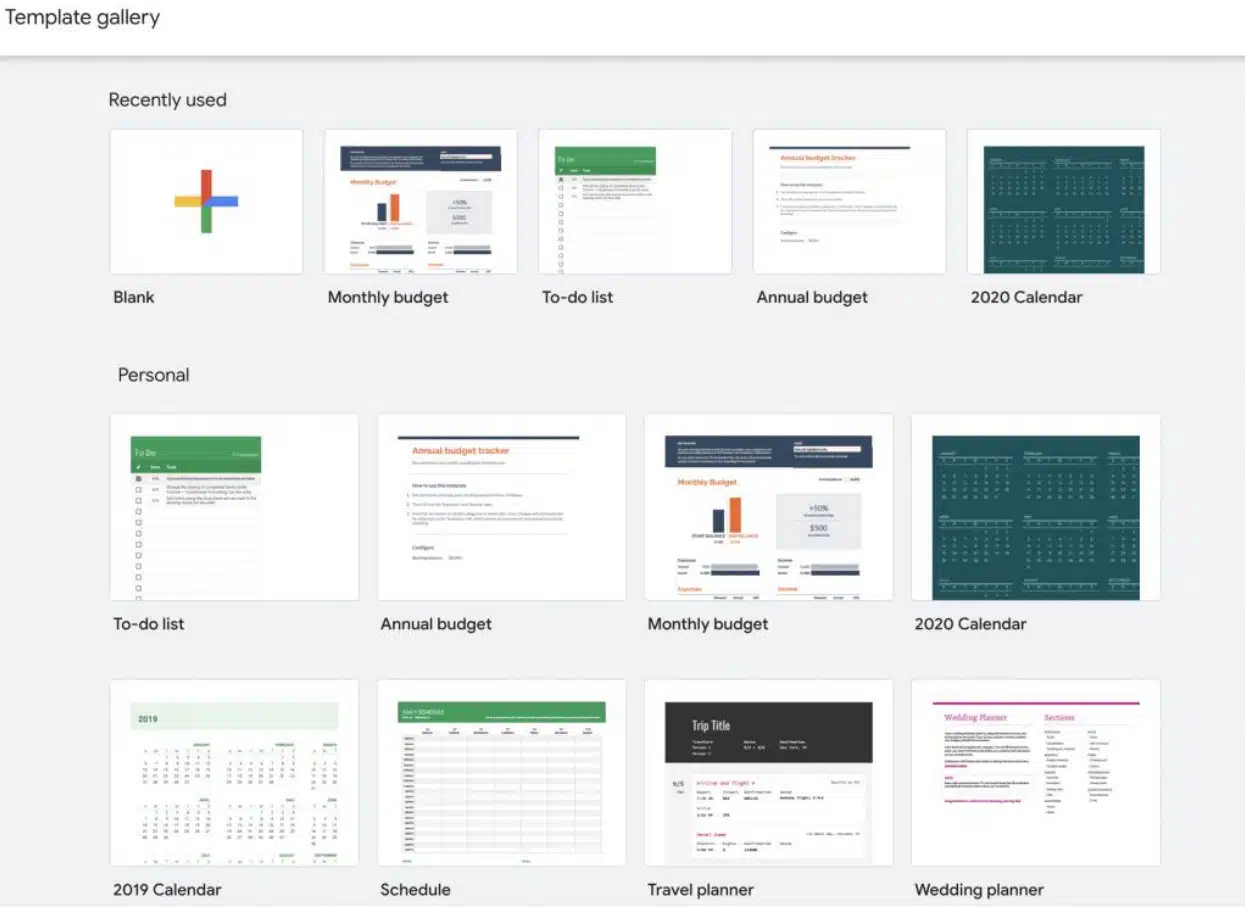

This will show you all of their pre built templates and you can select their monthly budget option in the middle.

3. DIY

DIY stands for “do it yourself” and is the practice of building or creating things on your own instead of buying an already finished product. IKEA, for example, made their entire business model around DIY furniture. You can get many IKEA products at about half the price of competitors since you can buy unfinished furniture, or even mix and match parts to create your own customized furniture.

Coffee is another excellent example of how you can DIY. Instead of buying Starbucks every morning for $3 a cup, you can buy a good coffee maker for $50 and a bag of organic coffee beans that can last you months for just $20. If you do this, you’d be breaking even on your investment in only 23 days, and everything after that is additional savings. But don’t just look to do this for coffee and furniture, DIY products are easy to make, and there are more options than you may think.

4. Buy Used Products

Whenever most of us need something new, our first impulse is to go straight to Amazon. This urge makes sense as they are the world’s largest marketplace. However, even though Amazon does a good job of getting us the products we want at affordable prices, we can do better.

For a lot of things like clothes and electronics, you can buy them used from eBay and local thrift stores. By buying slightly used products, you can get a stellar deal for practically no change in quality.

5. Put Your Savings In A Different Account

In today’s age, it is very easy for us to choose where we direct deposit our money. Instead of sending yourself the entirety of your check, take at least 5% and put it in a different account. A great place to put this 5% is with a financial services company like Vanguard or Fidelity and invest it in the stock market. Another option, if you don’t want to invest any of it, is to open up a separate bank account and have the money deposited there. And don’t tell me you don’t have 5% to spare because if you completed step 1, then you should already have much lower living expenses.

The trick to making this strategy work is never downloading the app to your savings account. Let’s say you open up a Chase account to deposit your 5%, don’t have the app on your phone. Just set up a percentage of your income to go to that app, set it, and forget it. You’ll thank yourself later when you find yourself sitting on a pile of cash you forgot you had.

6. Incentivize Savings Through Punishments & Rewards

Give yourself goals that you want to hit by a specific date that if you hit, you can get a reward. You can make this technique even more powerful if you also give yourself a punishment for falling short. For example, let’s say you want to save an extra $150 this month, and you have budgeted yourself accordingly so that you won’t have to sacrifice your current way of life.

If you successfully save the extra $150, reward yourself by buying yourself a pair of shoes you want at the end of the month. As a punishment, you can take an embarrassing photo of yourself and send it to your friend and say, “Post this photo on social media of me if I don’t cut back my spending this month by $150.”

This may be extreme, but it will be a strong motivator. Another example of what you could do is tell yourself if you don’t hit this goal, you have to donate to a foundation you don’t agree with, whether it’s political or what have you. This will be another great motivator to make sure you are on target with your money-saving goals.

7. Pay Off Debt

Unless used correctly, debt is a serious threat to your financial security. Now there are certain things in life where using debt can be advantageous like taking out a loan for college, a house, or a car. However, your goal should be to pay off your interest payments as quickly as possible so that it doesn’t suffocate you over the long term. This is especially true for credit card debt.

Credit card debt is some of the worst debt there is because most credit card issuers compound an account’s interest charges daily. If your debt interest compounds, that means the amount you owe will grow each time you don’t pay your payment. So over time, your payments will get larger and larger.

8. Leverage Credit Cards

Kind of oxymoronic to say “leverage credit cards” after just saying watch out for credit card debt. But as much as credit cards can hurt you, they can also be used to your advantage. As long as you aren’t spending above your means, credit cards can serve as an asset to help you on your path to financial freedom.

Most cards now offer incentives, so take advantage of the cards that offer cash back on purchases. Nerd Wallet has a great post on the Top Credit Cards of 2020 that you can check out to see which one might be best for you. Just remember to pay off your cards every month to keep your debt from piling up.

9. Get Paid Quicker

Everyone familiar with finance knows the importance of a company’s cash conversion cycle (CCC). In essence, your CCC is how quickly you get paid, vs. how often you have to pay. Managers want the lowest CCC possible as low conversion cycles mean that companies can get cash quickly and wait longer to pay off costs.

Now, why is that important for you? Because the reason why a low CCC is good for businesses is the same reason why a low CCC would be good for you. We should all strive to want to get paid before we have to pay for something so that we don’t have to use debt and incur interest charges.

Traditional pay periods don’t benefit us because we have to pay for expenses throughout the week, yet we only get paid bi-weekly. The only reason this is the case is that most companies only want to have to process payroll once every two weeks. However, bills, rent, and emergencies don’t always coincide with traditional pay periods.

Luckily, there is now an option for you to get paid quicker so that you don’t have to rely on credit cards and debt throughout the weeks. This option is DailyPay’s Digital Wallet Solution. This solution allows employees to access their pay and tips early and save it as they earn it.

No more waiting every two weeks to get paid, DailyPay’s Digital Wallet Solution puts you back in control and allows you to get paid on your terms.

10. Enjoy Life

Saving money is a lot like losing weight. If you starve yourself for a few weeks, you will see progress, but as soon as you get off that extremely strict diet, you go right back to your old eating habits. Saving money shouldn’t be something you dread like a strict diet but rather a lifestyle choice that you want to make. So if a $6 venti caramel macchiato from Starbucks puts a smile on your face, go out and buy one. Just keep it to once a week.

The key to any strategy you implement is moderation. If you never allow yourself to spend money on things you enjoy then you will never find a long term solution. But if you allow yourself windows of opportunity to splurge and buy things that bring you happiness then saving money won’t seem as treacherous of a task that everyone makes it out to be.